Fixed or Floating rate Home Loan for me?

With interest rates falling further and holding period for capital gains reduced from 3 to 2 years in the budget, new buyers and upgraders are looking to get the best realty deals. However, not all is done upon locating the property to buy. Choosing a right home loan product is vital to ensure that your hard earned money does not pay for exorbitant interest costs.

Home Loan – Product

A home loan comes with a variety of options and bargains but borrowers are not usually presented with all the available choices to make an informed choice. They are usually sold a product which may not suit them best. Let us take a case of a new buyer (or) an upgrader who seeks a loan of Rs.30 Lacs. This buyer is typically coerced into a 30-year “Fixed interest rate home loan” based on the lowest EMI option of Rs.23k per month. As this amount is close to the rental outgo of the buyer, s/he readily tends to accept the product.

A “Fixed” interest rate is in favor of the borrower if only the macro-economic condition is in a low interest rate era (2017). Longer tenure means lower EMI, but it also means higher interest payments to the bank. Shorter tenure means higher EMI, but an overall reduced interest outgo for the borrower.

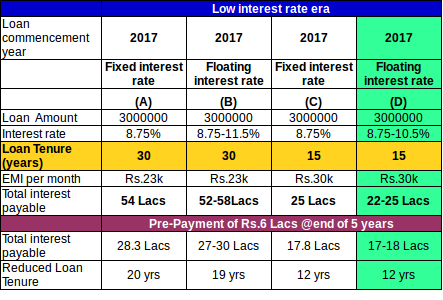

Low interest rate era

When we are borrowing in a low interest rate era as in 2017, then the interest outgo of fixed rate (A) & floating rate (B) is almost similar for a 30 year tenure. In either cases you’d be paying a whopping Rs.54 Lacs in interest on a Rs.30 Lacs loan. So, it is advisable to reduce the tenure to 15 years. If you do so, your EMI goes up from Rs.23k to Rs.30k p.m, while your total interest outgo is reduced from Rs.54 Lacs to Rs.25 Lacs, in cases (C) & (D) . Though in a low interest rate era, the difference in interest between (C) & (D) is not much, any further fall in interest rates could work to your advantage. So, pick a floating rate option with shorter tenure (D).

High interest rate era

If you were to borrow during a high interest rate era such as in 2013, then floating rate (Q) is way better than fixed rate (P) for a 30 year loan tenure. You may note that in fixed rate (P), you’d be paying Rs.50 Lacs interest (vs) the floating rate (Q) case, where you’d not only be paying a lower interest of Rs.37 Lacs, but you’d also be able to close your loan in 20 years. However, a prudent choice would be to go in for floating rate with lower tenure (S) to ensure you pay the least interest of Rs.25 Lacs on a Rs.30 Lacs loan and close your loan in 13 years. So, when you are in a high interest era too, it counts to choose a floating rate loan with a shorter tenure (S).

Could total interest outgo be reduced further?

When you get some handy cash or bonus, you may want to quickly make a pre-payment to your home loan. Pre-payments done within the first 1/3rd period of the loan tenure (Eg. in the 5th year for a 15yr loan tenure) significantly reduces your interest outgo. The above table shows that prepaying even Rs.6L (20% of loan) at the end of 5 years, helps to significantly lower both the interest outgo as well as loan tenure across all scenarios.

While pre-payments are allowed at ZERO charges in a floating rate product, fixed rate borrowers may be charged a 2-4% penalty on pre-payments, if it is not from their “own source” of funds. The reason is in the floating rate case, borrowers already bear the interest rate risks, while in the fixed rate case, the banks bear that risk and hence require to be compensated. However do note that the banks have made the pre-payment process quite painful for fixed rate borrowers. Another reason to pick a floating rate home loan.

Before signing up..

The interest rates on your bank FDs will tell you in which era of interest rates you are placed. Ensure to get a couple of amortization (home loan) quotations & check on pre-payment options before signing up with your bank/housing finance company. Then, pick the best quote with a lower tenure even if it means a slightly higher EMI initially (your salaries will only go up with time & you’ll learn to spend wisely). Just ensure to keep 6 months of EMI in a FD for any contingencies and buy a single premium home loan insurance to cover your loan amount. Alternatively, you could also consult your financial planner before choosing a home loan product. You’re then all set to sit back & enjoy your new home!

Leave a Reply